New white sedan at dealership lot with downward arrow symbolizing car depreciation

Car Depreciation Explained: How Vehicles Lose Value Over Time

Content

Content

Every vehicle begins losing value the moment its wheels leave the dealership lot. Understanding this inevitable financial reality helps you make smarter decisions whether you're buying new, shopping used, or planning when to sell. Car depreciation explained simply: it's the difference between what you paid and what you can sell for later—and that gap widens faster than most people expect.

The average new vehicle loses roughly 20% of its purchase price within the first 12 months. By year three, that same car retains only about 60% of its original sticker price. These aren't small numbers when you're talking about a $35,000 purchase that becomes worth $21,000 before your loan is even half paid off.

Depreciation isn't random. Specific patterns emerge across brands, vehicle types, and ownership circumstances. Some cars shed value like water off a windshield, while others hold strong for years. Knowing which factors accelerate losses—and which protect your investment—can save you thousands of dollars over your ownership period.

How Car Depreciation Works: The First Five Years

The depreciation curve vehicles follow isn't linear. Instead, it resembles a steep ski slope that gradually levels out. That first year delivers the hardest hit to your wallet, with new car value loss averaging 15-20% the instant you complete the purchase. Drive 10 miles home, and your $40,000 sedan is now worth roughly $32,000 to $34,000 if you tried selling it immediately.

Year two brings another 10-15% decline from the original price. By the end of year three, expect to retain only 55-65% of what you paid. The curve begins flattening around years four and five, when annual depreciation slows to 8-10%. After five years, most vehicles stabilize at 35-45% of their original MSRP.

Why does that first year hurt so much? Dealers and private buyers view any previously owned vehicle as "used," regardless of condition. The new-car warranty has been activated and partially consumed. Unknown factors enter the equation: Was it driven hard? Did the owner smoke inside? Even a flawless vehicle with 3,000 miles carries more questions than one sitting on the showroom floor.

| Year | Percentage of Original Value Lost | Remaining Value (%) | Example: $30,000 Car Value |

| 0 (New) | 0% | 100% | $30,000 |

| 1 | 20% | 80% | $24,000 |

| 2 | 30% | 70% | $21,000 |

| 3 | 40% | 60% | $18,000 |

| 4 | 48% | 52% | $15,600 |

| 5 | 55% | 45% | $13,500 |

These percentages shift based on make and model. A Toyota Tacoma might retain 70% after three years, while a luxury sedan from a less reliable brand could drop to 50% in the same timeframe. Market conditions also matter—the chip shortage of 2021-2023 temporarily reversed depreciation for many used vehicles, creating bizarre situations where two-year-old trucks sold for more than their original sticker price.

The steepest part of the curve exists because dealerships need profit margin on trade-ins. When you drive your brand-new purchase home, a dealer buying it back needs room to recondition, advertise, finance floor plan costs, and still make money on resale. That built-in spread explains much of the immediate value drop.

What Drives Your Car's Resale Value Up or Down

Resale value factors extend far beyond age and mileage. Brand reputation stands at the top of the list. Toyota and Honda consistently command higher resale prices because buyers trust their longevity. When someone shops for a used vehicle, they're betting on future reliability. A brand with documented quality ratings reduces that gamble.

Reliability ratings from Consumer Reports, J.D. Power, and similar organizations directly impact what buyers will pay. A model with a one-star reliability score scares away informed shoppers, forcing sellers to drop prices. Meanwhile, vehicles that routinely reach 200,000 miles without major repairs maintain stronger values throughout their lifespan.

Market demand creates surprising winners and losers. Full-size pickup trucks hold value exceptionally well in Texas and the Mountain West, where work and recreation require towing capacity. That same truck depreciates faster in dense urban markets where parking is scarce and gas prices sting harder. A Subaru Outback commands premium pricing in Colorado and Vermont but sits longer on lots in Florida.

Author: Kevin Thornton;

Source: shafer-motorsports.com

Condition and maintenance records separate similar vehicles by thousands of dollars. Two identical five-year-old sedans with 60,000 miles each can differ by $3,000 based purely on service history and cosmetic care. Buyers pay more for documented oil changes, tire rotations, and brake service. Conversely, deferred maintenance—worn tires, chipped paint, stained upholstery—signals neglect and triggers lowball offers.

Accident history haunts resale value even after perfect repairs. Carfax and AutoCheck reports reveal collision damage, and buyers immediately discount prices by 10-20% regardless of repair quality. The stigma persists because potential structural issues or future problems might emerge. Some buyers won't even consider vehicles with accident reports, shrinking your buyer pool.

Geographic location influences depreciation in unexpected ways. Convertibles lose value faster in Minnesota than California. Four-wheel-drive SUVs command premiums in mountain states but depreciate normally in flat regions. Salt-belt states (anywhere using road salt in winter) see faster depreciation on older vehicles due to rust concerns. A 10-year-old car from Arizona sells for more than an identical one from Michigan.

Seasonal timing affects what you can get. Convertibles sell for more in spring, trucks before winter, and fuel-efficient sedans when gas prices spike. Selling a two-wheel-drive sports car in January in Wisconsin means accepting a lower price than waiting until May.

"The biggest mistake car owners make is assuming depreciation is fixed. Your maintenance decisions, driving habits, and even where you park can swing your vehicle's resale value by 15-20% compared to an identical model owned differently. Depreciation isn't something that happens to you—it's partly under your control." — Brian Moody, Executive Editor, Kelley Blue Book

— Kevin Thornton

Mileage vs. Age: Which Hurts Your Car's Value More?

The depreciation by mileage versus age debate has no universal answer—it depends on the numbers involved. Generally, age matters more for the first five years, while mileage dominates the equation for older vehicles. A three-year-old car with 75,000 miles (25,000 per year) raises more red flags than a five-year-old with the same mileage.

High-mileage newer cars suggest commercial use, rideshare service, or long commutes. Buyers worry about accelerated wear on suspension components, transmissions, and interiors. A 2022 sedan with 90,000 miles in 2024 likely spent its life on highways, which is actually easier on vehicles than city driving—but buyers don't always think that through. The age suggests it should have 30,000-40,000 miles, so the excess triggers suspicion and lower offers.

Low-mileage older cars present different concerns. A 2015 vehicle with only 20,000 miles sounds appealing until you consider the implications. Was it driven so infrequently that seals dried out? Did it sit outside for months at a time? Short trips without reaching operating temperature cause more engine wear than highway miles. Tires age regardless of mileage, and rubber components deteriorate from time alone.

Author: Kevin Thornton;

Source: shafer-motorsports.com

The "sweet spot" for resale combines reasonable age with slightly below-average mileage. Americans drive roughly 12,000-15,000 miles annually on average. A five-year-old vehicle with 50,000-60,000 miles hits the target: used enough to stay mechanically sound, not so much that major services loom. Buyers feel comfortable with that profile.

Commercial versus personal use dramatically affects depreciation. Former rental cars, fleet vehicles, and rideshare cars depreciate faster even with identical mileage and age. Buyers assume these vehicles experienced harder use, more drivers with varying skill levels, and less emotional attachment to proper care. A rental car history can knock 10-15% off resale value compared to a single-owner personal vehicle.

Odometer readings carry more weight as vehicles age. For a two-year-old car, being 5,000 miles over average barely registers. For a 10-year-old vehicle, the difference between 100,000 and 150,000 miles significantly impacts value. Major service intervals (timing belts, transmission fluid, spark plugs) cluster around 100,000 miles for many vehicles. Crossing that threshold means buyers face immediate maintenance costs.

Vehicle Types That Lose Value Fastest (and Slowest)

Luxury sedans from German manufacturers rank among the fastest depreciating cars. A BMW 7 Series or Mercedes S-Class can lose 60-70% of its value in five years. The reasons stack up: expensive maintenance and repairs scare budget-conscious used car shoppers, technology becomes outdated quickly, and the prestige factor diminishes once the model isn't current. A $90,000 luxury sedan becomes a $30,000 used car faster than almost any other vehicle type.

Full-size SUVs from domestic brands also depreciate rapidly, particularly when gas prices rise. A Chevrolet Suburban or Ford Expedition loses value quickly because fuel costs make them expensive to operate. When gas hits $4-5 per gallon, buyers flee large SUVs, flooding the market and driving prices down.

Electric vehicles occupy complicated territory. Early EVs like the Nissan Leaf depreciated catastrophically—70-80% in five years—due to limited range, battery degradation concerns, and rapid technology improvements. Why buy a used EV with 80 miles of range when new models offer 250+ miles?

Author: Kevin Thornton;

Source: shafer-motorsports.com

Pickup trucks, especially from Toyota and certain Ford and RAM models, hold value remarkably well. The Toyota Tacoma famously retains 60-70% of its value after five years. Strong demand from contractors, outdoor enthusiasts, and those needing towing capacity keeps prices high. Limited supply (trucks take longer to build than sedans) also supports values.

Jeep Wranglers defy normal depreciation rules. Their unique capability, removable tops and doors, and cult following mean five-year-old Wranglers often retain 60-65% of original value. The used market stays strong because Wrangler buyers specifically want that vehicle, not just "any SUV."

Sports cars vary wildly. Mass-market sports cars (Ford Mustang, Chevrolet Camaro) depreciate normally, while limited-production models or those with racing pedigree can actually appreciate. A base Mustang loses 50% in five years; a Mustang Shelby GT350 might lose only 25%.

Minivans depreciate faster than crossovers despite similar utility. The stigma of "family hauler" limits buyer interest once kids grow up. Honda Odyssey and Toyota Sienna hold value better than Chrysler Pacifica, but all minivans lose 55-60% in five years.

Electric Vehicles: A Special Depreciation Case

Battery degradation represents the biggest concern for used EV buyers. Lithium-ion batteries lose capacity over time and charge cycles. A five-year-old EV might have 85-90% of its original range, which sounds acceptable until you realize that 250-mile range is now 215 miles. Range anxiety intensifies with used EVs.

Technology obsolescence hits EVs harder than gas vehicles. A 2018 electric car's infotainment system, charging speed, and battery management software feel ancient compared to 2024 models. Gas engines haven't fundamentally changed—a 2018 V6 works essentially like a 2024 V6—but EV technology leapt forward dramatically.

Tax credit impacts on used pricing create market distortions. New EV buyers received up to $7,500 in federal tax credits, effectively reducing purchase price. Used EV buyers didn't qualify (until recently with smaller credits), but sellers still lost that $7,500 from resale value. If you paid $40,000 after tax credit for a car with $47,500 MSRP, you can't expect buyers to pay based on the $47,500 figure.

Battery replacement costs loom over older EVs. Replacing an EV battery costs $5,000-$15,000 depending on model. Once an EV reaches 8-10 years old, buyers factor in potential battery replacement, tanking values. A 10-year-old gas car might need a transmission eventually ($3,000-$4,000), but a 10-year-old EV faces battery anxiety that's harder to quantify.

Charging infrastructure improvements also hurt older EV values. Early EVs used slower charging standards. Newer fast-charging networks don't support older models, or charge them much slower. This practical limitation makes older EVs less appealing.

The car you drive doesn’t define your worth. But understanding what your car is worth — and why — defines how wisely you spend your money

— Dave Ramsey

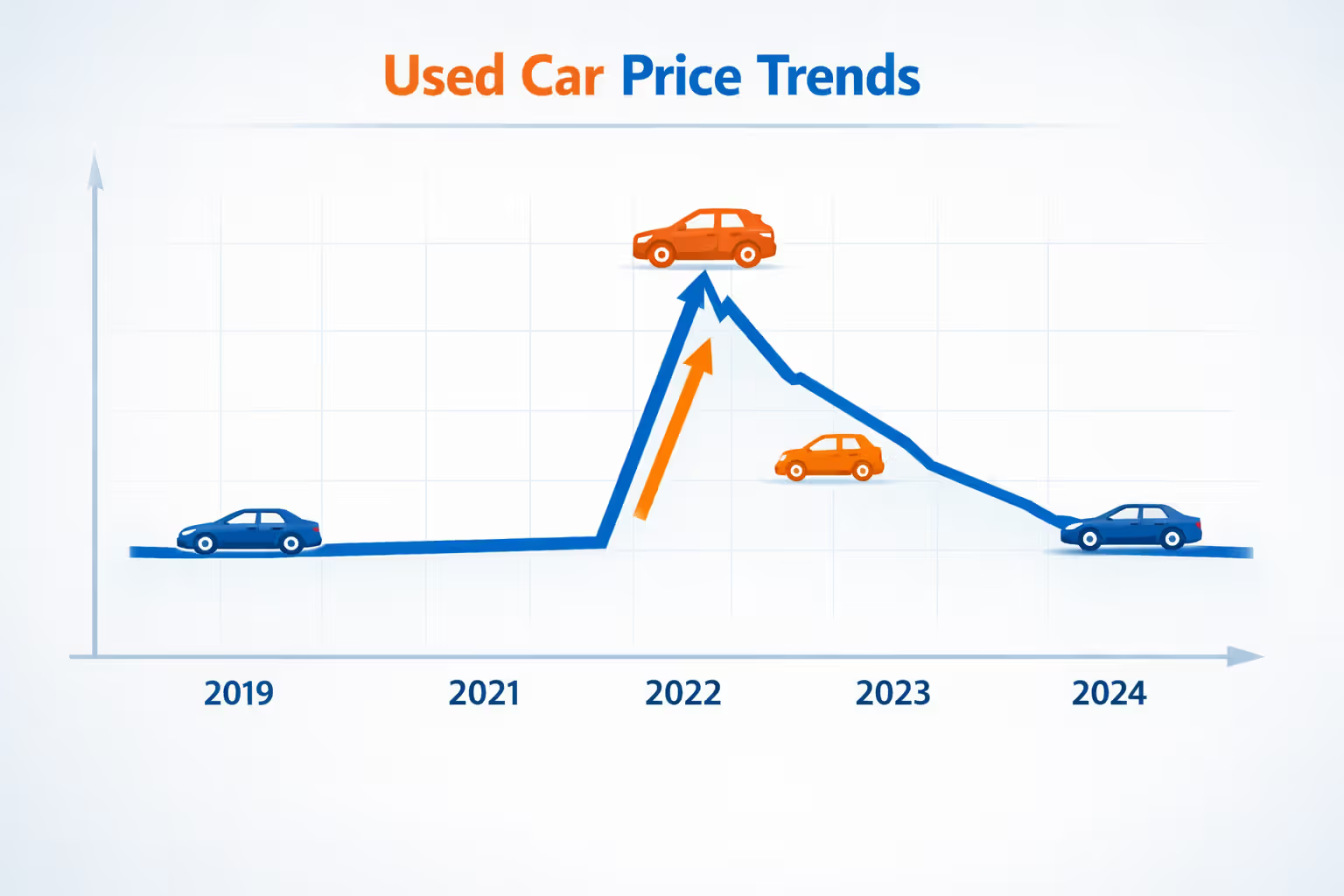

How Current Market Trends Are Changing Used Car Prices

Post-pandemic pricing shifts disrupted decades of predictable depreciation patterns. When semiconductor shortages halted new vehicle production in 2021-2022, used car pricing trends reversed entirely. Used vehicles appreciated instead of depreciated. Two-year-old trucks sold for more than their original sticker prices. The normal rules suspended temporarily.

That bubble deflated through 2023-2024 as production recovered, but used prices remain elevated compared to pre-pandemic levels. A three-year-old vehicle that would have sold for $18,000 in 2019 now commands $22,000-$24,000 even as the market normalizes. Inflation, higher new vehicle prices, and sustained demand keep used prices above historical averages.

Supply chain effects continue influencing the new versus used equation. When new car inventory sits at 30-40 days (below the healthy 60-day supply), buyers turn to used vehicles, supporting prices. Conversely, when dealers accumulate excess inventory, they discount new vehicles, making used cars less attractive and accelerating depreciation.

Author: Kevin Thornton;

Source: shafer-motorsports.com

Interest rates dramatically impact depreciation through financing costs. When rates jumped from 3% to 7-8% in 2022-2024, monthly payments on used vehicles increased substantially. A $25,000 used car at 3% over 60 months costs $449/month; at 7% it's $495/month. That $46 difference pushes some buyers toward cheaper vehicles, softening demand for higher-priced used cars and accelerating depreciation.

Lease returns flooding the market affect specific segments. Luxury brands lease heavily—60-70% of German luxury vehicles are leased. When those three-year leases mature, dealerships get flooded with off-lease inventory, depressing used luxury prices. This predictable cycle means luxury depreciation accelerates in years with high lease return volumes.

Electric vehicle adoption rates influence depreciation. As charging infrastructure expands and range anxiety decreases, used EV values stabilize. The $4,000 used EV tax credit introduced in 2023 also supports values by effectively reducing buyer cost.

Smart Strategies to Minimize Depreciation Loss

Timing your purchase around the depreciation curve offers the biggest savings. Buying a two-to-three-year-old vehicle captures most of the utility while avoiding the steepest value loss. Someone else absorbed that brutal first-year 20% hit. You get a nearly-new vehicle with modern features, remaining warranty, and 60-70% of its life ahead for 70-80% less than new.

The absolute worst time to buy is brand new unless you plan to keep the vehicle 10+ years. If you trade every 3-5 years, you're perpetually eating the steepest part of the depreciation curve. Let someone else take that hit.

The moment you settle for less than you deserve, you get even less than you settled for. In car buying, that means never ignoring the math of depreciation

— Suze Orman, Personal Finance Expert and Author

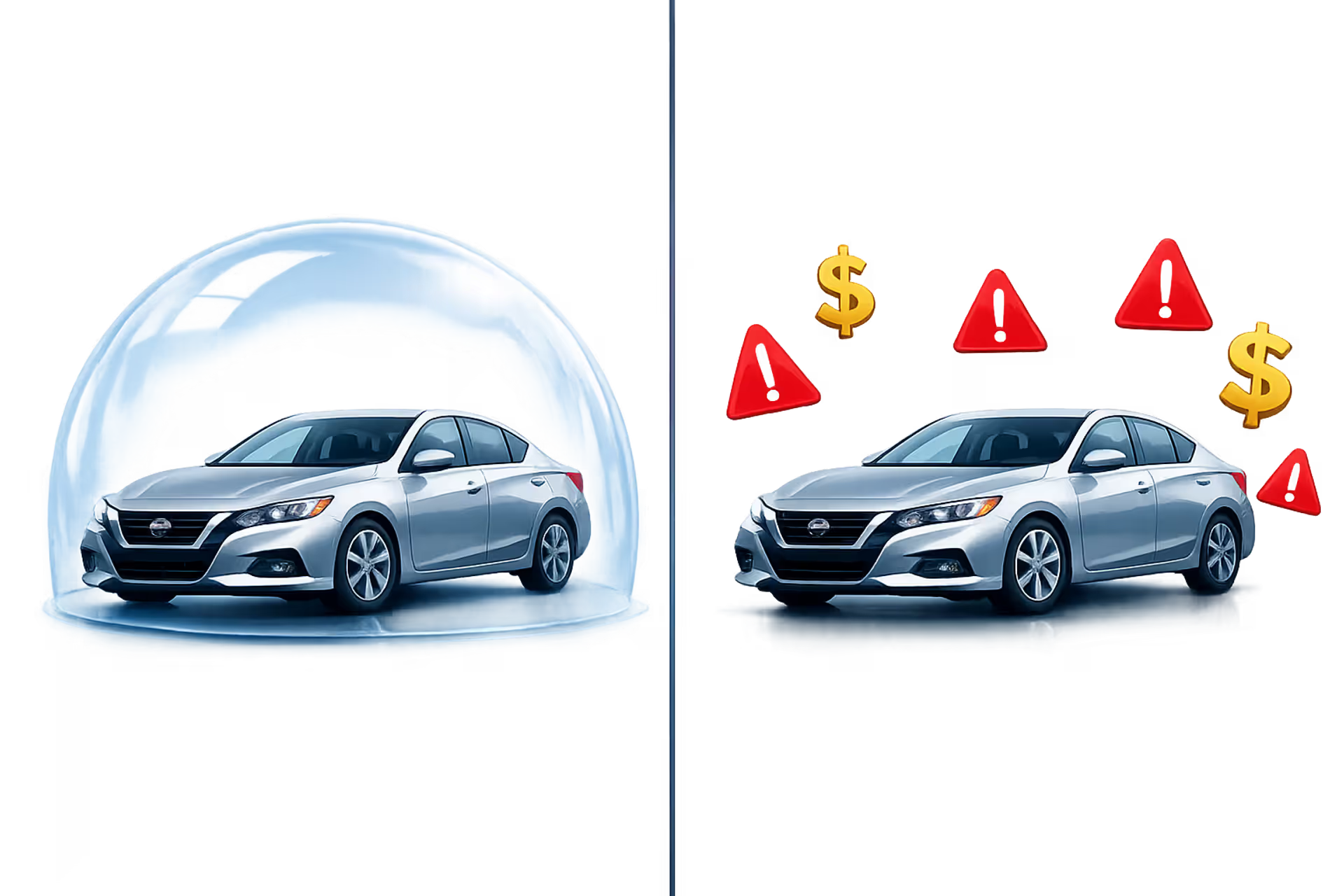

Maintenance decisions directly impact resale value. Following the manufacturer's service schedule and keeping records adds $1,000-$2,000 to resale value. Skipping services to save $500 now costs you $1,500 later. Regular washing and interior cleaning, paint touch-ups on chips, and addressing minor issues before they become major problems all protect value.

Modifications almost always hurt resale value. That $3,000 aftermarket exhaust system or $2,000 suspension lift appeals to a narrow buyer segment while turning off mainstream buyers. You might recover 30-40% of modification costs. The only exception: adding features the vehicle should have had—backup cameras on older cars, remote start in cold climates—can break even or slightly increase value.

Lease versus buy considerations center on depreciation. Leasing makes sense if you want a new vehicle every three years, because you're only paying for the depreciation during your lease term. Buying makes sense if you keep vehicles 7+ years, allowing you to drive through the depreciation curve into the stable, low-depreciation years.

Choosing brands and models with strong resale value costs more upfront but saves money long-term. A Toyota Camry priced $2,000 higher than a comparable Nissan Altima will retain $3,000-$4,000 more value after five years. You're actually ahead by buying the more expensive vehicle.

Color choices matter more than most realize. Neutral colors (white, black, gray, silver) appeal to the broadest audience and hold value better. Bright or unusual colors (yellow, orange, bright green) limit your buyer pool. Boring wins when it comes to resale.

Avoiding the first model year of a redesigned vehicle protects you from depreciation spikes if quality issues emerge. First-year models often have bugs that get fixed in year two. If major recalls or problems surface, first-year models depreciate faster.

Frequently Asked Questions About Car Depreciation

Making Depreciation Work for You

Understanding depreciation transforms how you approach vehicle ownership. It's not just about the purchase price—it's about total cost of ownership across your intended timeline. A $30,000 vehicle that retains $15,000 in value after five years costs you $15,000 in depreciation alone, before gas, insurance, or maintenance. A $35,000 vehicle that retains $22,000 costs only $13,000 in depreciation despite the higher purchase price.

The buyers who come out ahead either keep vehicles long enough to drive through the steep depreciation curve (8-10+ years), or buy used vehicles at 2-4 years old and sell at 5-7 years during the flatter part of the curve. The worst financial decision is buying new and trading every 3-4 years—you perpetually absorb the steepest losses.

Depreciation also creates opportunities. Luxury vehicles that depreciated heavily become accessible to budget-conscious buyers willing to handle higher maintenance costs. Three-year-old luxury SUVs priced 40-50% below original MSRP deliver premium features for mainstream money.

Your specific circumstances should drive decisions. If you drive 30,000+ miles annually, buying new and keeping long-term makes sense because you'll accumulate high mileage quickly regardless. If you drive 8,000 miles per year, buying a low-mileage used vehicle maximizes value since you'll add miles slowly.

Depreciation is the largest ownership cost for most vehicles, exceeding fuel and maintenance combined. Treating it as a strategic consideration rather than an unavoidable fact puts thousands of dollars back in your pocket over your lifetime of vehicle ownership.

Related Stories

Read more

Read more

The content on Auto Insights is provided for general informational and educational purposes only. It is intended to offer guidance on car buying, vehicle ownership, finance, insurance, EVs, maintenance, accessories, reviews, and related topics, and should not be considered professional financial, legal, insurance, mechanical, or investment advice.

All information, tools, calculators, comparisons, and recommendations presented on this website are for general guidance only. Individual financial situations, driving habits, vehicle conditions, insurance policies, and market factors vary, and actual results or costs may differ from estimates provided.

Auto Insights makes no guarantees regarding accuracy, completeness, or current applicability of the information, as automotive markets, regulations, incentives, interest rates, and vehicle specifications may change over time.