Flat lay of a wooden desk with a laptop showing a car affordability calculator, car keys, bank statements, a calculator, dollar bills, and a pen

How Much Car Can I Afford? Calculate Your Budget in 3 Steps

Walk into any dealership and you'll hear the same question: "What monthly payment works for you?" It's the wrong question. Dealers don't ask about your take-home pay, your student loans, or whether you've budgeted for $200 monthly insurance premiums. They want a number they can hit, even if it means stretching you to a 72-month loan.

Here's what happened to my neighbor last year: approved for a $42,000 SUV on his $65,000 salary, excited about the $580 payment. Six months in, he was picking up weekend shifts because insurance came in at $240—not the $140 he estimated—and premium gas was bleeding him dry. The payment was manageable. The total cost of driving that SUV every day? Unsustainable.

You need three actual numbers before you shop: what you'll put down, what you'll pay monthly, and what the entire ownership experience will cost. Not what sounds reasonable. Not what gets approved. What the math actually supports when you write it all out.

Author: Derek Fulton;

Source: shafer-motorsports.com

The 20/4/10 Rule and Other Car Affordability Formulas

Financial planners throw around different benchmarks depending on who's asking. Someone with zero debt has more flexibility than someone juggling three credit cards and a mortgage. Let's break down what each formula actually measures.

The 20/4/10 Rule sets the tightest boundaries. You're putting 20% cash down upfront, financing over four years maximum, and capping everything—loan payment, insurance, gas, maintenance—at 10% of what you earn before taxes. Take someone pulling in $75,000 yearly. That's $6,250 monthly before anything gets withheld. Ten percent means $625 total. Insurance and gas eat up $250? Your payment tops out at $375. Run that through a loan calculator at 6% for 48 months and you're financing maybe $16,000. Add your 20% down and you're shopping in the $20,000 range.

The 10-15% Gross Income Rule only looks at your loan payment, ignoring everything else. Same $75,000 earner could justify a $625 payment at the 10% mark, or $937 if they push to 15%. This feels more generous until your insurance company quotes you $220 monthly, premium fuel runs another $180, and you're already over the 20/4/10 threshold before counting oil changes.

The 36% Debt-to-Income Threshold matters because it's what mortgage lenders use, and car lenders pay attention too. Every monthly debt obligation combined—mortgage, student loans, car payments, credit card minimums—needs to stay under 36% of gross income. Already carrying 28% between your mortgage and student loans? You've got 8% left for a car, period. On $75,000 that's $500 monthly, regardless of what payment-only formulas suggest you can handle.

Which one applies to your situation? Debt-free with cash reserves? The 20/4/10 rule keeps you conservative. Carrying a mortgage and other obligations? Start with the 36% ceiling and work backward from there. The 15% payment approach only works if your insurance is cheap, you're debt-light, and you drive something economical—maybe you're 45 with a clean record in Nebraska buying a Honda Civic. For a 25-year-old in Miami financing a Charger? That's a recipe for drowning.

Step-by-Step: Calculate Your Maximum Car Price

Abstract formulas mean nothing until you plug in your actual bank statements and paychecks. Here's the sequence that reveals your real number.

Factor in Your Monthly Income and Existing Debts

Pull up your gross monthly income first—the amount before taxes, health insurance, and retirement contributions come out. Paid every two weeks? Take one check, multiply by 26 annual pays, divide by 12 months. Count guaranteed bonuses if they're contractual, but skip the occasional commission windfall.

Now list every recurring monthly debt: mortgage or rent, student loans, car loans on a vehicle you're keeping, credit card minimum payments (not what you usually pay, the actual minimum), personal loans, alimony. Total those up. Divide that sum by your gross monthly income to get your current debt-to-income ratio. Subtract from 36% to find your remaining borrowing capacity for a car payment.

Real example: You gross $5,500 monthly. Mortgage runs $1,200, student loan $280, credit card minimums $150. That's $1,630 in debt, or 29.6% DTI. You've got 6.4% remaining breathing room, which translates to $352 monthly for a car payment. Not $500. Not $600. $352.

Too many people buy a car they can afford on paper but can’t afford in life. The real cost of a vehicle is never just the monthly payment — it’s everything that follows it

— Dave Ramsey

Determine Your Down Payment Capacity

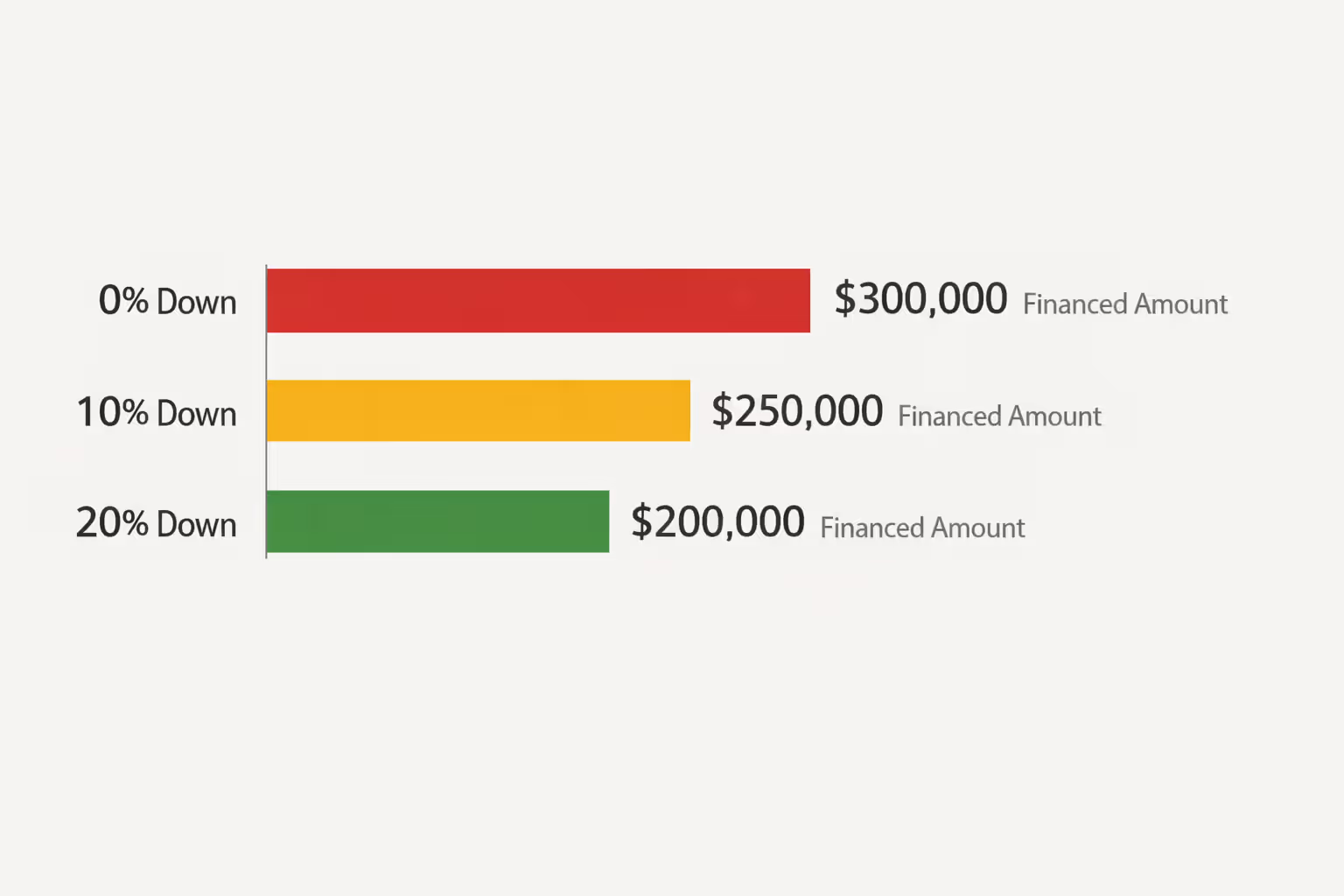

Look at your checking and savings. What can you pull for a down payment without touching your emergency fund? Twenty percent down is textbook ideal, but plenty of solid used car buyers put down 10-15%. Drop below 10% and you're immediately underwater—you owe more than the car's worth—which becomes a crisis if it gets totaled or you need to move on in two years.

Trading in your current car? Get three dealer quotes and check Kelley Blue Book for the trade-in value, not private party. Subtract whatever you still owe on that car loan. The difference is your usable equity. A car worth $12,000 with $9,000 left on the loan gives you $3,000 equity toward your next purchase.

Let's say you've scraped together $2,000 cash and have that $3,000 trade equity. You're at $5,000 total down payment. Want to hit the 20% threshold? Your ceiling is $25,000 purchase price. Comfortable going to 10% down? You could look at $50,000—but now you're financing $45,000, and we haven't even discussed what that monthly payment becomes or whether you have room for it in your DTI.

Author: Derek Fulton;

Source: shafer-motorsports.com

Estimate Insurance, Maintenance, and Ownership Costs

Call your insurance agent or run online quotes for the specific models you're considering before you commit. Two $28,000 cars can differ by $120 monthly in premiums. A Honda Accord and a Dodge Charger aren't remotely comparable in insurance costs, even at identical purchase prices. Financing requires full coverage—comprehensive and collision—which runs higher than liability-only.

Fuel costs depend on your commute and driving habits, but figure $100-150 monthly if you're doing typical 12,000 annual miles in something getting 25 mpg with gas at $3.50 per gallon. Set aside another $100-150 for maintenance and repairs. New cars under warranty need less upfront, but you're still looking at oil changes, tire rotations, and eventual brake work. Used cars past 80,000 miles? Budget the higher end.

Stack everything together. Your $400 loan payment plus $180 insurance, $120 gas, and $100 maintenance equals $800 monthly vehicle expense. Does that fit the 10% rule for your income? Earning $8,000 gross monthly? You're fine. Earning $6,000? You're $200 over budget every single month, and that's assuming nothing breaks.

Income vs. Car Price: What Can You Actually Afford?

Here's what different income levels actually support under each formula. These calculations assume 10% down payment, 6% interest rate, 48-month financing, with $150 monthly insurance and $100 combined for gas and basic maintenance.

| Annual Gross Income | Conservative 20/4/10 Limit | 10% Payment Rule Limit | 15% Payment Rule Limit |

| $40,000 | $18,000 | $22,000 | $34,000 |

| $50,000 | $23,000 | $28,000 | $42,000 |

| $60,000 | $27,000 | $33,000 | $51,000 |

| $75,000 | $34,000 | $42,000 | $63,000 |

| $100,000 | $46,000 | $56,000 | $85,000 |

| $125,000 | $57,000 | $70,000 | $106,000 |

Look at the gap at $60,000 annual income. Conservative approach says $27,000 maximum. The looser 15% payment approach lets you nearly double that to $51,000. What's the difference? Financial cushion. That $51,000 car leaves you zero margin when the transmission needs work, you lose your job, or rates jump if you need to refinance. The $27,000 purchase keeps your budget flexible enough to absorb surprises without panic.

These numbers also assume minimal other debt. Carrying $30,000 in student loans? That's $300-400 monthly in payments, which directly reduces how much car you can afford. Your realistic maximum drops $10,000-15,000 from these figures. You can't ignore existing obligations and pretend you're starting from a clean slate.

How Lenders Determine Your Auto Loan Limits

Pre-approval letters feel like permission to spend up to that amount. They're not. They're a lender's calculation of the maximum loan you can technically service based on income and credit—not what leaves you financially healthy. Lenders make money on interest. Approving you for the biggest possible loan is literally how they maximize profit.

Debt-to-Income Ratio: Lenders often approve loans up to 43-50% total DTI, well above the 36% financial advisors recommend. They'll greenlight a loan pushing you to 48% DTI because technically you can make the payments. But that leaves almost nothing for retirement contributions, emergency savings, or basic quality of life. You're approved, not comfortable.

Credit Score Impact: A 720+ credit score might land you 5-6% APR. Drop to 620 and you're looking at 10-14%. Finance $30,000 over 60 months at 6% versus 12%—the difference is $100 monthly and $6,000 total interest over the loan life. Lower scores also trigger higher insurance premiums in most states, compounding your monthly burden.

Loan-to-Value Ratio: Lenders cap how much they'll loan relative to the car's value. New cars might get 110-125% LTV to roll in taxes and dealer fees. Used cars typically top out at 100-110%. Buying a $25,000 car with nothing down? They might approve $27,500 to cover fees and taxes. You're immediately $2,500+ upside down, which means you can't sell or trade without writing a check to cover the negative equity gap.

Why Pre-Approval Amounts Mislead: You get approved for $40,000 based on stated income and credit score. The lender doesn't know you're spending $200 monthly on credit cards, $150 on a consolidation loan, and $100 on subscriptions that auto-renew. They calculated 30% DTI. Your actual reality is 40%. Taking that full $40,000 loan doesn't stretch you—it buries you.

Author: Derek Fulton;

Source: shafer-motorsports.com

5 Mistakes That Lead to Buying Too Much Car

Ignoring Total Cost of Ownership: You fixate on the $450 monthly payment and completely forget insurance, gas, and maintenance will add $350. Suddenly your vehicle costs $800 monthly, not $450, and your budget implodes. Luxury badges and performance cars amplify this trap—premium fuel requirements, expensive OEM parts, higher insurance brackets. A $35,000 BMW costs vastly more to own than a $35,000 Honda.

Stretching Loan Terms: A 72-month loan makes a $35,000 car seem affordable at $550 per month versus $730 over 48 months. But you'll pay $4,600 more in interest, and you'll be underwater for four years. When the transmission fails in year four, you owe $18,000 on a car worth $12,000. You're trapped—can't sell, can't trade, can't escape without taking a massive loss.

Skipping the Down Payment: Zero-down promotions are marketed as customer perks. They're financial traps. You owe more than the car's value from day one, your monthly payment runs higher, and you pay significantly more interest over the loan term. Can't afford a down payment? You genuinely cannot afford that car, regardless of what gets approved.

Forgetting About Trade-In Equity: Dealers inflate trade values to make deals look attractive, then quietly bury the difference in your new loan. You think they gave you $15,000 for your trade, but you owed $13,000 on it—your actual equity is $2,000. They financed the new car's full price minus $2,000, not minus $15,000. Always read the contract line by line to see where your trade equity actually went.

Lifestyle Inflation: You get a $10,000 raise and immediately upgrade your car payment by $400 monthly. But that raise should first increase your retirement contributions, build your emergency fund, and accelerate debt payoff. A $10,000 salary increase nets about $625 monthly after taxes. Spending $400 on a nicer car leaves $225 for everything else that matters for building wealth.

"The biggest mistake I see is people calculating affordability based solely on the monthly payment they can squeeze into their budget right now, without accounting for insurance increases, maintenance, or any life changes. A car payment is a multi-year commitment, and your income or expenses might not stay static." — Jennifer Schultz, CFP, Certified Financial Planner

— Derek Fulton

Using an Affordability Calculator: What the Logic Actually Tells You

Online calculators prompt you for income, existing debts, down payment amount, estimated interest rate, and desired loan term. They calculate a maximum car price. The logic is straightforward: determine your available monthly budget after other debts, calculate the corresponding loan amount at the given rate and term, then add your down payment to reach a purchase price.

Which Inputs Matter Most: Monthly income and existing debt obligations control everything else. A $500 difference in monthly debt payments shifts your maximum affordable price by $15,000-20,000. Interest rate matters less for affordability—it moves your max price by 5-10%—but dramatically affects total interest paid over the loan. The difference between 5% and 9% on a $30,000 loan is $3,000+ in interest.

Limitations: Calculators don't know your specific life circumstances. They can't account for irregular income, upcoming major expenses like weddings or tuition, or your personal risk tolerance. They assume you'll keep the car for the entire loan term and that your insurance quote is accurate. They won't warn you when you're pushing into genuinely risky territory that looks acceptable on paper.

How to Interpret Results: Treat the calculator's maximum price as a ceiling, never a target. Calculator says you can afford $40,000? Shop for $32,000-35,000 instead. That $5,000-8,000 buffer absorbs surprises: insurance quotes coming in higher than estimated, unexpected repairs on a used car no longer under warranty, or several months of reduced income if work slows down.

A budget is telling your money where to go instead of wondering where it went. That applies to car buying more than almost any other financial decision

— John C. Maxwell

Run multiple scenarios through the calculator. What happens if you increase your down payment by $2,000? What if you choose a 36-month term instead of 60? The calculator shows trade-offs between loan term, down payment size, and maximum purchase price. A shorter loan term means higher monthly payments but drastically less interest paid and faster equity building. Play with the variables until you understand what drives your specific situation.

FAQ: Car Affordability Questions

Conclusion

Figuring out your actual car budget isn't about what gets approved or what monthly payment you can technically swing. It's about choosing a number that keeps your finances stable when life throws surprises, your stress manageable, and your options open for other financial goals that matter.

Start with the 20/4/10 rule as your foundation, adjust for existing debts and available down payment, and always calculate the complete cost of ownership—not just the sticker price or payment. Run your real numbers honestly. If the car you want pushes you past 36% DTI or requires a six-year loan to make the payment work, it's too much car for your situation right now.

A slightly older model year, different trim level, or competing brand often saves $5,000-10,000 and makes the difference between comfortable and constantly stretched. The right car fits your budget today and twelve months from now, even if your income drops temporarily or your expenses increase unexpectedly. That's what real affordability looks like.

Related Stories

Read more

Read more

The content on Auto Insights is provided for general informational and educational purposes only. It is intended to offer guidance on car buying, vehicle ownership, finance, insurance, EVs, maintenance, accessories, reviews, and related topics, and should not be considered professional financial, legal, insurance, mechanical, or investment advice.

All information, tools, calculators, comparisons, and recommendations presented on this website are for general guidance only. Individual financial situations, driving habits, vehicle conditions, insurance policies, and market factors vary, and actual results or costs may differ from estimates provided.

Auto Insights makes no guarantees regarding accuracy, completeness, or current applicability of the information, as automotive markets, regulations, incentives, interest rates, and vehicle specifications may change over time.