Car partially submerged in water as a visual metaphor for an underwater car loan with negative equity

Negative Equity Car Loan: What It Means and How to Get Out of It

Content

Content

You've been sending those car payments every single month like clockwork. Maybe even set up autopay so you never miss one. Yet if you walked into a dealership tomorrow trying to trade that car, you'd discover something unsettling: the payoff amount your bank demands is thousands higher than what anyone will actually give you for the vehicle.

Recent industry data shows roughly one in five financed vehicles currently sits in this predicament. The math creates a trap—your loan balance towers above the car's actual market price, which finance folks describe as being "underwater" or "upside down." You can't easily switch to different transportation, and if someone totals your car in an accident, the insurance settlement could leave you holding a bag of debt.

Let's break down exactly why this happens to millions of drivers, and more importantly, I'll show you the practical moves that actually work to escape it.

What Is Negative Equity on a Car Loan?

Here's the core concept: you've got negative equity when the amount you still owe exceeds what your car would sell for today. Let's say your sedan has a fair market value of $18,000, but when you call your lender for a payoff quote, they tell you $22,000. That $4,000 gap? That's your negative equity—and you're responsible for covering it. The upside down car loan meaning is just another way people describe this exact same financial situation.

This creates immediate headaches the second you want to exit that vehicle. Your lender holds the title as collateral and won't release it until receiving complete payment. A dealer might happily offer you $18,000 as a trade-in value, but your bank won't accept anything less than the full $22,000 payoff. You've got to come up with that missing $4,000 somehow, or you're stuck driving what you've got.

Look at Sarah's real-world situation. Two years back, she bought a new SUV stickered at $42,000, managed only a tiny down payment, and financed nearly the entire purchase. Fast forward to today—her loan payoff sits at $35,000, but that SUV's trade-in value dropped to just $28,000. She's carrying $7,000 of negative equity. When her family situation changes and she needs a minivan instead? She either writes a seven-thousand-dollar check or keeps driving the SUV whether it works for her or not.

Breaking Down Different Equity Scenarios

| Scenario | Car Value | Loan Balance | Equity Position | Status |

| Good situation | $25,000 | $18,000 | +$7,000 | You've built equity |

| Dead even | $21,500 | $21,500 | $0 | Neither good nor bad |

| Moderate trouble | $19,000 | $24,000 | -$5,000 | You're underwater |

| Serious trouble | $16,000 | $28,000 | -$12,000 | You're deeply underwater |

Look at that top row—when you've built positive equity, you've got options and freedom. You can trade up, trade down, or sell whenever circumstances change. That bottom row? Your hands are completely tied until somehow eliminating that deficit.

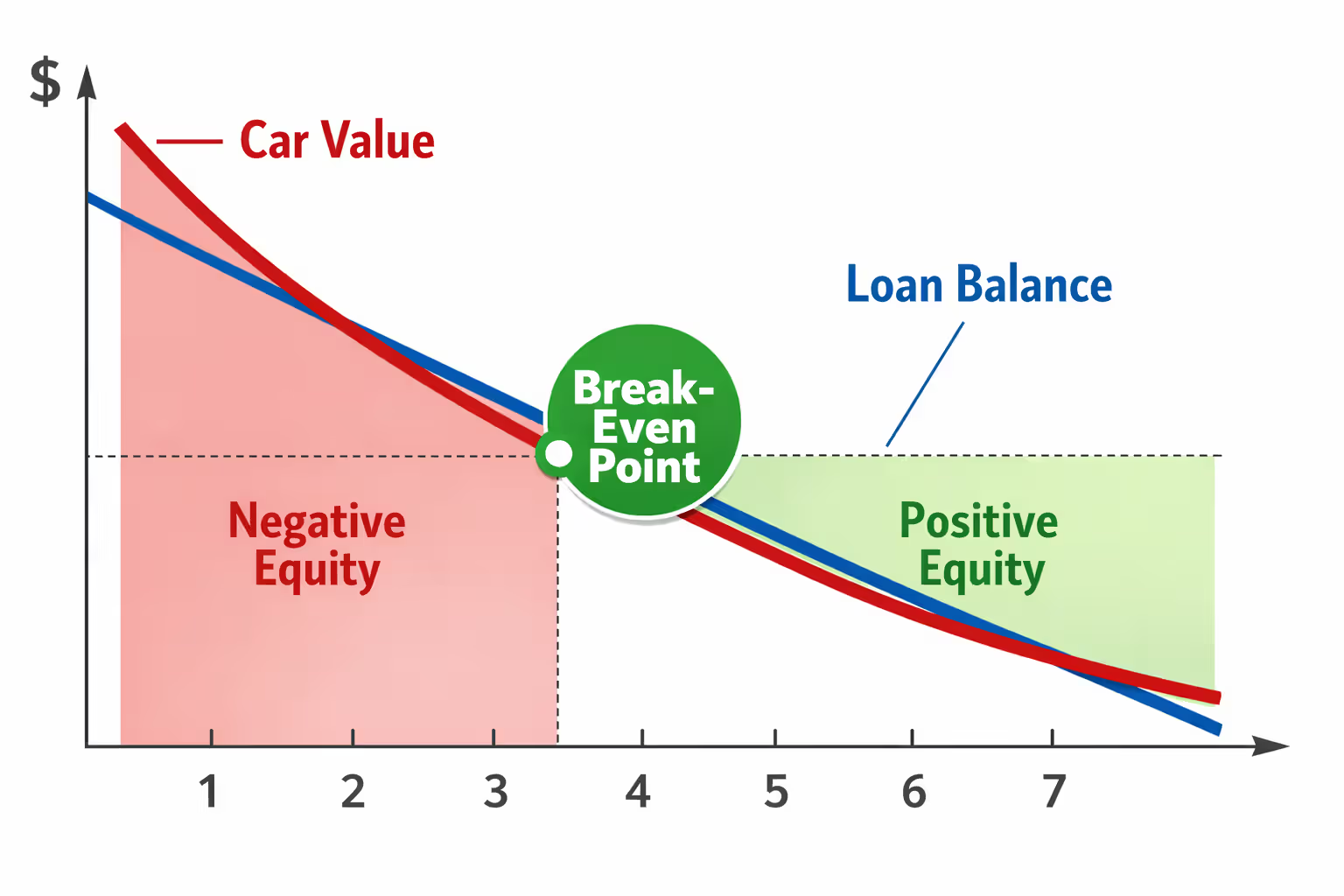

How Does a Car Loan Become Upside Down?

New cars lose value shockingly fast right after purchase. Drive a $40,000 vehicle off the lot and it sheds somewhere between $8,000 and $12,000 of value during just the first year—that money evaporates into nothing. Meanwhile, your loan balance barely budges because those early payments funnel mostly toward interest rather than principal. You might send in $5,000 worth of payments during year one while the actual loan balance drops by only $2,000.

Zero-down financing arrangements start you in a hole from day one. You finance the complete purchase price plus taxes, registration fees, dealer documentation charges, maybe an extended warranty—suddenly you've borrowed $38,500 for something the market values at $32,000 the moment you drive it home. You're underwater before accumulating a single mile.

Extended loan terms—those 72-month or 84-month payment plans—create problems in slow motion. Sure, spreading payments across six or seven years makes the monthly number more manageable for your budget. But you're barely touching the principal. Two years into a six-year loan, maybe you've knocked down 25% of what you borrowed while the vehicle plummeted 40% in value. The math simply works against you.

Beware of little expenses; a small leak will sink a great ship

— Benjamin Franklin

High interest rates make everything worse. Borrow $30,000 at a 12% annual rate and roughly $3,000 of your first year's payments goes entirely to interest. That money accomplished exactly nothing toward building equity—it just enriched your lender.

Rolling previous negative equity forward creates a compounding disaster. You owed $5,000 more than your old car was worth and the dealer convinced you to fold it into your new loan? Congratulations, you started $5,000 behind before the new vehicle lost a single dollar to depreciation. I've watched borrowers repeat this cycle—rolling $5,000, then $7,000, then $10,000 into consecutive purchases. A decade passes and they've funneled massive amounts to lenders without ever building actual wealth.

Calculating Your Current Equity Position

The equity calculation auto loan uses simple arithmetic: current market value minus remaining loan balance equals equity. If the answer comes out positive, you're doing fine. If the answer is negative, you're underwater.

Getting accurate numbers for loan balance vs value takes two separate steps. Your current payoff amount shows up on monthly statements, appears in your lender's app, or you can get it through a quick customer service call. Ask specifically for the payoff amount—this includes accrued interest and any settlement fees, making it different from your current balance.

Figuring out current market value means checking multiple sources because estimates vary wildly between them. Hit Kelley Blue Book, Edmunds, and NADA Guides—all offer free valuations you can access in minutes. Be brutally honest about condition. Those door dings, the stained back seat, 50,000 miles on the odometer instead of 30,000—these details hammer value hard. Use trade-in values if you're considering dealer transactions, not private party prices, because trade-in shows what dealerships actually pay.

Where you live matters more than most people expect. A four-wheel-drive pickup commands premium prices in Minnesota but it's just another truck in Arizona. Check what identical vehicles actually sold for recently in your area using Autotrader, CarGurus, or Cars.com.

Walking Through an Equity Calculation Step by Step

James owns a 2021 sedan with 42,000 miles showing. He logs into his auto loan account and finds his payoff amount: $19,750. Next he hits the valuation websites:

- KBB trade-in estimate: $17,200

- Edmunds trade-in: $16,800

- NADA trade-in: $17,500

Averaging these three gives him $17,167 as a realistic trade value. Now the math: $17,167 minus $19,750 equals negative $2,583. James is carrying $2,583 in negative equity. If he wants to trade that sedan for something else? He's either writing a check to cover the shortfall or rolling it into new financing.

Run this calculation every six months. Watch your progress as payments chip away at the balance and depreciation eventually slows down. You'll hit break-even eventually, then finally climb into positive territory.

Author: Brianna Lowell;

Source: shafer-motorsports.com

Financial Risks of Staying in Negative Equity

Getting stuck with a vehicle you can't unload without taking a financial hit creates real complications. Your family expands and that two-door coupe stops making sense. Your job situation changes and that $550 payment starts choking your budget. Negative equity kills your flexibility to adapt without swallowing substantial losses.

Total loss scenarios get scary fast. Insurance companies pay actual cash value when your car gets totaled—not whatever you still owe. Say you're $6,000 underwater when someone runs a red light and T-bones your car. Insurance sends the market value payment to your lender, but you still owe that remaining $6,000. Except now you're making payments on scrap metal sitting in a salvage yard. You need replacement transportation AND you're still covering payments on the destroyed vehicle.

Trading or upgrading becomes basically impossible unless you roll that deficit into new financing, which usually means taking on even bigger debt loads. Most dealers cap rolled negative equity somewhere between $5,000 and $7,000 depending on your credit. Underwater beyond that ceiling? You're locked in until paying it down.

The wealth destruction compounds over years in ways borrowers don't immediately see. Money trapped servicing negative equity could be funding your retirement account, building emergency savings, or knocking out credit card balances. Staying underwater for years potentially costs tens of thousands in missed opportunities.

Can You Refinance a Car Loan with Negative Equity?

Refinancing while underwater is possible, just tougher than normal. Lenders typically won't refinance beyond 125% of your vehicle's value. Your car's worth $20,000? The maximum refinance loan most will approve is $25,000. Owe more than that threshold and your application gets rejected automatically.

When does refinance negative equity actually make sense? If your credit score jumped significantly since you signed the original loan, you might qualify for dramatically better rates. Dropping from 14% APR down to 7% creates real savings across whatever loan term remains, even while underwater. Just calculate the genuine interest savings against any refinancing fees before pulling the trigger.

Your credit score controls everything here. Lenders willing to refinance negative equity usually demand 650 minimum, with the best rates reserved for scores above 700. They're taking on extra risk by lending more than the collateral's worth, so they compensate through stricter borrower requirements.

Evaluate the potential savings carefully against the risks you're accepting. Refinancing typically extends your loan duration, meaning you stay underwater longer. You've got 30 months left on a 60-month loan and you refinance into a fresh 48-month term? You just reset your timeline. Meanwhile depreciation keeps grinding away.

Here's an alternative approach: hold off on refinancing and instead hammer the principal with extra payments for six to twelve months. Once you've wrestled that loan-to-value ratio down to 120% or less, you'll qualify for better refinancing terms with multiple lenders competing for your business.

Author: Brianna Lowell;

Source: shafer-motorsports.com

Rolling Negative Equity Into Your Next Car Purchase

Here's how rolling negative equity trade in actually works: you owe $23,000 on your current car but it's only worth $19,000 at trade-in. The dealer pays off your entire $23,000 loan to satisfy the lender, then tacks that $4,000 difference straight onto your new vehicle's purchase price. You're financing the shortfall right alongside the new car.

Dealers usually allow rolling between $5,000 and $7,000 in negative equity, though this fluctuates based on your credit profile and which vehicle you're buying. Luxury brands or high-profit vehicles give dealers more room to absorb negative equity. Economy cars running on thin profit margins leave almost zero flexibility.

That rolled negative equity destroys your new loan structure. You're financing debt completely disconnected from the vehicle you're actually driving, and it accumulates interest at your full loan rate. Sitting at 8% APR? You're paying interest on phantom value. Your monthly obligation jumps, your loan-to-value ratio starts terrible immediately, and you're instantly deep underwater on a brand new vehicle.

This tactic usually makes your position worse rather than better. You're grabbing negative equity from one depreciating asset and slapping it onto another depreciating asset. Unless your income increases substantially or you plan keeping the new vehicle until it literally disintegrates, you're just perpetuating the same cycle.

When might rolling actually make practical sense? Your current vehicle constantly breaks down and repair bills are bleeding you dry—getting into something reliable might justify accepting rolled negative equity. Or maybe you relocated somewhere your two-wheel-drive sedan can't handle winter conditions and you genuinely need different transportation. Sometimes it's your only realistic option.

Proven Strategies to Eliminate Negative Equity

Throwing extra money toward principal every month gives you the most direct escape route. Even adding $100 or $200 monthly directly attacks the balance. On a $25,000 loan at 7% APR, adding just $150 extra each month cuts roughly 18 months off your term and saves over $1,500 in interest while building equity considerably faster.

Verify absolutely that those extra payments hit principal rather than advancing future payment due dates. Some lenders automatically process overpayments as prepayment of next month's bill, which accomplishes nothing for accelerating balance reduction. Contact your lender or check their online portal to confirm you're designating principal-only payments.

Selling privately and covering the deficit yourself works when you've got available cash. Private party sales typically generate $2,000 to $4,000 more than dealer trade-in offers. You're $3,000 upside down? Selling privately might only require covering $1,000 from your own pocket. You'll coordinate directly with your lender to handle title transfer and payoff, which adds complexity but preserves real money.

Sometimes patience is your smartest play if you can afford keeping the car. Vehicle depreciation slows dramatically after year three. A car that hemorrhaged 40% of value during the first three years might only drop another 10% across the next two years. Meanwhile, your monthly payments keep reducing the balance. Time eventually brings you to break-even, then into positive equity.

Author: Brianna Lowell;

Source: shafer-motorsports.com

Gap insurance protects against catastrophe but doesn't solve your negative equity situation. It covers the difference between insurance payout and loan balance if your car gets totaled, preventing you from owing money on destroyed property. However, it won't help you trade or sell, and coverage ends when your policy expires. Think of gap insurance as disaster protection, not an exit strategy.

The secret of getting ahead is getting started

— Mark Twain

Avoid mistakes that dig deeper holes: Never skip payments assuming minimal consequences. Late payments trigger fees and trash your credit score, making refinancing harder or impossible. Don't pile on more debt by financing expensive repairs or accessories through your auto loan. And don't assume leasing your next vehicle solves anything—most lease companies won't absorb significant negative equity either.

Frequently Asked Questions About Negative Equity Car Loans

Moving Forward with Negative Equity

Finding yourself underwater doesn't sentence you to permanent financial distress. Consistent monthly payments combined with slowing depreciation and strategic extra payments gradually bring your loan balance in line with your vehicle's value. Most borrowers who resist the temptation to roll negative equity into new purchases hit break-even within three to four years.

Focus your energy on factors you control: make consistent on-time payments, skip unnecessary modifications or add-ons that don't boost resale value, maintain the vehicle properly to preserve its worth, and apply any financial windfalls—tax refunds, work bonuses, side income—directly toward principal reduction.

Shopping for your next vehicle? Use this experience to dodge repeating the same cycle. Put at least 20% down in cash, choose loan terms of 60 months maximum, and consider buying slightly used rather than brand new to skip the steepest depreciation cliff. These steps keep you in positive equity from the beginning and provide flexibility when life circumstances inevitably change.

Understanding exactly where you stand financially with your vehicle puts you in control rather than constantly reacting to problems. Run your equity calculation today, review your loan terms carefully, and create an actual plan to either accelerate payoff or position yourself for better refinancing opportunities. The sooner you tackle negative equity head-on, the sooner you'll have real options with your transportation needs instead of feeling trapped.

Related Stories

Read more

Read more

The content on Auto Insights is provided for general informational and educational purposes only. It is intended to offer guidance on car buying, vehicle ownership, finance, insurance, EVs, maintenance, accessories, reviews, and related topics, and should not be considered professional financial, legal, insurance, mechanical, or investment advice.

All information, tools, calculators, comparisons, and recommendations presented on this website are for general guidance only. Individual financial situations, driving habits, vehicle conditions, insurance policies, and market factors vary, and actual results or costs may differ from estimates provided.

Auto Insights makes no guarantees regarding accuracy, completeness, or current applicability of the information, as automotive markets, regulations, incentives, interest rates, and vehicle specifications may change over time.