Car key on extended warranty service contract document with calculator and dollar bills on desk

Is an Extended Warranty Worth It? A Data-Driven Analysis for Car Owners

Extended warranties cost between $1,200 and $4,500 depending on your vehicle. Most owners will never file a claim that exceeds what they paid upfront. That single fact shapes the entire economics of these contracts, yet dealerships sell them to roughly 50% of new car buyers.

The question isn't whether extended warranties provide value to someone—it's whether they provide value to you. Your answer depends on your vehicle's failure patterns, your financial cushion, and how you weigh predictable costs against unpredictable ones. This analysis walks through the numbers, exclusions, and scenarios that determine when these contracts make sense and when they're expensive peace of mind you don't need.

How Extended Warranties Actually Work (And What They Don't Tell You)

An extended warranty isn't technically a warranty—it's a service contract. This distinction matters because warranties are included with your purchase and regulated as part of the vehicle sale, while service contracts are separate insurance-like products with their own terms, administrators, and claim processes.

When you buy one at a dealership, three parties are typically involved: the selling dealer, the contract administrator (often the finance company processing your paperwork), and the actual provider who pays claims. If the provider goes bankrupt, your contract may become worthless even though you bought it from a trusted dealer. This happened to customers of American Auto Shield and U.S. Direct Protect in recent years.

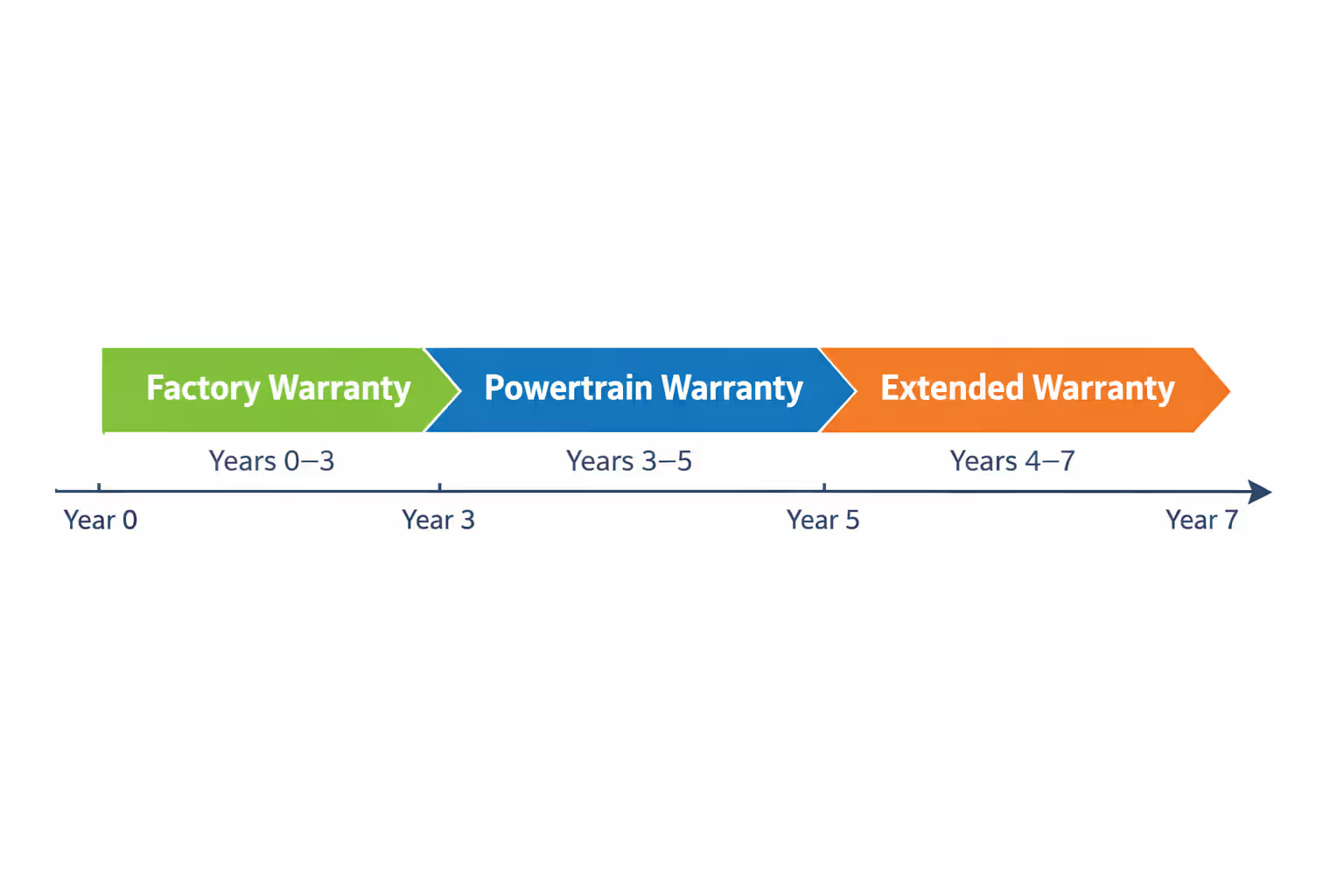

Coverage Periods vs. Manufacturer Warranties

New vehicles come with a factory warranty, typically three years or 36,000 miles for comprehensive coverage and five years or 60,000 miles for powertrain components. Extended service contracts pick up where these end, though many are sold while factory coverage is still active.

You'll see coverage described in terms like "7 years/100,000 miles from the original in-service date" or "4 years/48,000 miles from the date of purchase." That first type starts counting from when the car was first sold as new, not when you bought the extended contract. If you're buying a two-year-old car with a "7-year" extended warranty, you're actually getting five years of potential coverage.

Author: Lena Prescott;

Source: shafer-motorsports.com

What "Bumper-to-Bumper" Really Means

Marketing materials love this phrase, but actual contracts never cover everything between the bumpers. The most comprehensive service contract value still excludes maintenance items, wear components, and anything the provider can attribute to lack of upkeep.

"Stated component" contracts list exactly what's covered—typically 30 to 60 specific parts. "Exclusionary" contracts flip this model, covering everything except a listed set of exclusions. The second type sounds better but often contains exclusion lists running several pages. Both approaches leave substantial room for claim denials based on interpretation.

Contracts also distinguish between mechanical breakdown and failures caused by external factors. If your transmission fails because of an internal defect, you're covered. If it fails because you ignored a leaking seal that contaminated the fluid, the contract administrator will cite lack of maintenance. The burden of proof often falls on you to demonstrate you followed the maintenance schedule exactly.

The Real Math: Calculating Your Break-Even Point

Extended warranties are priced so the provider profits after paying claims and administrative costs. That's not inherently bad—all insurance works this way—but it means the average buyer pays more than they receive. The question is whether you'll be average or an outlier who benefits.

Start with this formula: (Warranty Cost + Deductibles) < (Probability of Major Failure × Average Repair Cost)

If a $2,500 extended warranty has a $100 deductible per visit, and you expect to file three claims over the coverage period, you need those repairs to total more than $2,800 to break even. For most vehicles, major repairs (transmission, engine, electrical system) cost $2,000 to $5,000 each, so a single catastrophic failure can justify the contract. Two or three smaller failures rarely will.

| Vehicle Type | Avg. Warranty Cost | Avg. Repair Costs (Years 4-7) | Break-Even Probability | Recommendation |

| Economy Sedan (Honda Civic, Toyota Corolla) | $1,400 | $800 | 15% chance of major failure | Skip it |

| Midsize SUV (Ford Explorer, Chevy Traverse) | $2,200 | $1,600 | 35% chance of major failure | Marginal—depends on model year |

| Luxury Sedan (BMW 5-Series, Mercedes E-Class) | $4,200 | $5,800 | 58% chance of major failure | Worth considering |

| Full-Size Truck (Ford F-150, Ram 1500) | $2,600 | $1,900 | 28% chance of major failure | Skip unless high mileage |

These figures assume you're buying coverage that extends from year 4 through year 7 of ownership. Repair probability cost increases significantly after 100,000 miles, when wear-related failures compound mechanical ones. If you plan to keep your truck for 200,000 miles, the math shifts in favor of the warranty—but only if the contract actually covers that duration.

The dealer's finance office won't show you this table. They'll emphasize the cost of a single transmission replacement ($4,500) without mentioning that your specific vehicle has a 7% chance of needing one during the coverage period. They'll finance the warranty into your loan, making a $2,500 contract cost $3,200 after interest over five years.

Author: Lena Prescott;

Source: shafer-motorsports.com

What Extended Warranties Won't Cover: Reading the Fine Print

Warranty exclusions explained in plain terms: more claims get denied for coverage gaps than for any other reason. You'll discover these gaps when you're already facing a repair bill, not when you're signing the contract.

Pre-existing conditions are excluded universally. If your check engine light was on before you bought the contract, any related repairs won't be covered. Third-party warranty companies often request a pre-purchase inspection, but dealer-sold contracts rarely do—they'll simply deny claims retroactively by arguing the problem existed at purchase.

Maintenance-related failures create the most disputes. Miss an oil change, and your engine failure gets denied. Use aftermarket parts instead of OEM components, and your claim gets rejected. The contract requires you to maintain receipts proving every scheduled service. One missing receipt for a $40 cabin air filter can void a $3,000 claim if the administrator argues that neglected maintenance contributed to the failure.

Wear items are never covered. This includes brake pads, rotors, wiper blades, batteries, tires, and clutches. But the definition of "wear" gets murky. Is a leaking shock absorber a wear item or a mechanical failure? Contract language leaves room for interpretation, and that interpretation favors the provider.

Specific high-cost exclusions appear in fine print: damage from overheating, even if the cooling system failed first; failures caused by "lack of coolant or lubricant," regardless of why fluids were low; anything related to rust, corrosion, or environmental damage; and all electronics not specifically listed as covered (which, in modern vehicles, is nearly everything).

One common scenario: your turbocharger fails. The contract covers turbochargers, so you file a claim. The administrator's inspector determines the failure was caused by contaminated oil. They deny the claim, stating that contamination indicates you used improper oil or extended change intervals. You have receipts proving you followed the schedule exactly, but the oil brand you used isn't on their approved list—a list you didn't know existed. You're now liable for a $2,800 repair.

The best warranty is a reliable car. The second best warranty is a savings account dedicated to repairs

— Clark Howard

Vehicle Reliability as Your Primary Decision Factor

Vehicle reliability risk analysis should determine 80% of your decision. Some brands engineer vehicles that rarely experience expensive failures during the extended warranty period. Others have documented patterns of costly breakdowns that make coverage a reasonable bet.

High-Reliability Brands That Rarely Justify Extended Coverage

Toyota, Lexus, Honda, and Mazda consistently rank at the top of reliability studies. Their vehicles are engineered with conservative tolerances and proven components. A 2019 study tracking repair costs found that Toyota Camry owners spent an average of $420 on non-maintenance repairs between years 4 and 7 of ownership. No extended warranty at $1,200+ makes financial sense against that baseline.

Subaru and certain Hyundai/Kia models also demonstrate strong reliability, though specific model years matter. The 2015-2018 Subaru Outback has minimal reported issues, while the 2010-2014 models experienced head gasket failures that would justify coverage.

Author: Lena Prescott;

Source: shafer-motorsports.com

If you drive a reliable vehicle, your money compounds better in an index fund than in a service contract. A $2,000 warranty premium invested at 7% annual returns grows to $2,800 over five years—enough to cover the average repair and leave you with a surplus.

Models With Known Expensive Failure Points

German luxury brands—BMW, Mercedes-Benz, Audi, Porsche—have complex engineering and expensive parts. A BMW 5-Series owner faces a 58% probability of a repair exceeding $2,000 between years 4 and 7. Common failures include water pumps ($1,800), valve cover gaskets ($1,400), and electronic control modules ($2,500+). The repair probability cost for these vehicles makes extended coverage worth evaluating.

Certain American vehicles with specific powertrains also warrant consideration. The Ford Explorer with the 3.5L EcoBoost engine (2011-2019) has documented failures of the water pump, turbos, and timing chain components. Repair costs easily exceed $3,000. The Chevrolet Traverse (2009-2017) experiences timing chain and transmission issues that justify coverage for high-mileage drivers.

Chrysler, Jeep, and Ram vehicles consistently rank near the bottom of reliability studies. A Jeep Grand Cherokee owner faces significantly higher repair probability than a Toyota Highlander owner. If you're committed to these brands for other reasons (capability, preference, existing ownership), an extended warranty shifts from "probably not worth it" to "reasonable risk management."

Smarter Alternatives to Extended Warranties

Ownership risk planning doesn't require purchasing a service contract. Several strategies provide financial protection without the limitations and profit margins built into extended warranties.

Self-insurance through a dedicated repair fund works for most reliable vehicles. Open a high-yield savings account and deposit what you would have spent on a warranty—say, $50 monthly if you'd have paid $1,800 for a three-year contract. After 18 months without a major repair, you have $900 saved. After three years, you have $1,800 plus interest. If you never need a major repair, you keep the money. If you do need one, you've got funds available without deductibles or claim denials.

This repair budgeting strategy requires discipline. You can't raid the fund for other expenses. But it gives you flexibility: if your water pump fails and costs $600, you pay it and continue building the fund. An extended warranty with a $100 deductible would cover $500 of that repair, but you've already paid $1,800 for the contract.

Manufacturer-certified pre-owned warranties often provide better value than third-party extended contracts. CPO programs from Toyota, Honda, Lexus, and others include thorough inspections, coverage that matches or exceeds factory warranties, and claims processed directly by the manufacturer. You're not dealing with a third-party administrator looking for reasons to deny. CPO warranties are typically available only at purchase, so negotiate them into the deal.

Credit card extended warranty benefits double the manufacturer's warranty up to one additional year on many premium cards. If your vehicle has a three-year factory warranty, certain cards extend it to four years at no cost beyond your annual fee. This doesn't help with older vehicles, but it's a free benefit many owners overlook.

Independent mechanic relationships reduce repair costs 30-50% compared to dealership rates. An extended warranty typically requires repairs at approved facilities, often limiting you to dealers. If you've built a relationship with a trustworthy independent shop, you'll pay $800 for a repair that would cost $1,500 at a dealer. Over time, this difference exceeds what you'd save with a warranty.

Risk comes from not knowing what you’re doing. In car ownership, that means not knowing what your specific vehicle is likely to cost you

— Warren Buffett

When an Extended Warranty Actually Makes Sense

Certain ownership scenarios tilt the math toward purchasing coverage, even accounting for the built-in profit margin.

Luxury and European vehicles with documented expensive repairs justify extended warranties if you plan to keep the car past factory coverage. A $4,000 extended warranty on a BMW 5-Series becomes reasonable when a single repair (valve body replacement, $3,800) would otherwise deplete your emergency fund. You're paying a premium for predictable budgeting.

High annual mileage drivers—those exceeding 20,000 miles yearly—accelerate wear and increase failure probability. If you'll hit 150,000 miles within the coverage period, repair probability cost rises significantly. Ensure the contract's mileage limit accommodates your usage; a "7 years/100,000 miles" warranty becomes worthless at 100,001 miles, even if you're only in year five.

Limited emergency fund situations create a legitimate use case. If a $2,500 repair would force you to carry credit card debt at 22% interest, a $1,800 extended warranty provides a safety net. You're paying for financial stability, not mathematical optimization. This only makes sense if you're simultaneously working to build that emergency fund—the warranty is a temporary bridge, not a permanent solution.

Transferable warranty scenarios add resale value. Some contracts transfer to subsequent owners, making your vehicle more attractive to buyers. A used car with two years of remaining extended warranty coverage can command a $500-$800 premium. If you paid $2,200 for the warranty, used it for three years, and recovered $700 at resale, your net cost drops to $1,500.

According to consumer advocate John Paul, AAA Northeast's Car Doctor: "Extended warranties make sense for about 20% of car buyers—those with vehicles that have higher-than-average repair costs, those who drive significantly above average miles, or those who genuinely can't absorb a major repair bill. For everyone else, you're better off being your own insurance company."

FAQ: Extended Warranty Questions Answered

Making Your Decision: A Framework

Extended warranties aren't inherently good or bad—they're risk transfer mechanisms with built-in profit margins. Your decision should follow this framework:

First, identify your vehicle's reliability profile. Look up repair frequency and average costs for your specific make, model, and year. If you own a Toyota Corolla, skip the warranty and invest the money. If you own a Jeep Grand Cherokee, move to the next step.

Second, calculate your actual break-even point using realistic repair probabilities for your vehicle, not hypothetical worst-case scenarios. A $2,500 warranty needs to save you more than $2,500 in repairs, including deductibles and claim denials.

Third, review your financial situation honestly. If you have $5,000 in accessible savings and could absorb a major repair without hardship, you don't need the predictability an extended warranty provides. If a $2,000 surprise would create financial stress, the warranty serves a legitimate purpose beyond pure mathematics.

Fourth, read the actual contract, not the sales brochure. Identify the exclusions, required maintenance documentation, approved repair facilities, and claim process. If the contract requires you to get pre-approval before repairs and your car breaks down on a Saturday, how does that work? If you can't understand the terms, don't buy it.

Finally, negotiate hard if you decide to purchase. Extended warranties have enormous markup—often 50-80% profit margin for the dealer. Offer half the quoted price. If they won't negotiate, walk away. You can usually purchase the same coverage later, and third-party providers sell comparable contracts for less.

The majority of car owners are better off building their own repair fund and accepting the uncertainty that comes with vehicle ownership. But if you've worked through this framework and an extended warranty addresses a specific risk you're not comfortable bearing, buying one isn't irrational—it's just expensive peace of mind. Make sure you understand exactly what you're paying for.

Related Stories

Read more

Read more

The content on Auto Insights is provided for general informational and educational purposes only. It is intended to offer guidance on car buying, vehicle ownership, finance, insurance, EVs, maintenance, accessories, reviews, and related topics, and should not be considered professional financial, legal, insurance, mechanical, or investment advice.

All information, tools, calculators, comparisons, and recommendations presented on this website are for general guidance only. Individual financial situations, driving habits, vehicle conditions, insurance policies, and market factors vary, and actual results or costs may differ from estimates provided.

Auto Insights makes no guarantees regarding accuracy, completeness, or current applicability of the information, as automotive markets, regulations, incentives, interest rates, and vehicle specifications may change over time.